Key Points

-

Lululemon has long been at the forefront of the athleisure fashion industry.

-

When you simplify the company’s approach, it’s basically a luxury clothing store.

-

Individuals considering the recent decline in value should be aware of what they are purchasing and the reasons behind it.

-

10 stocks we prefer over Lululemon Athletica Inc. ›

Lululemon Athletica (NASDAQ: LULU)has a devoted fan base, with stores that are frequently packed with shoppers. This is positive for the company, but what exactly is the business? At first glance, Lululemon offers fitness apparel. However, when you check the prices on its garments, it’s evident that the items it sells are high-end products.

Here are three key points you should know before purchasing the stock.

1. Style is the main influence

Lululemon doesn’t produce everyday clothing. While it’s true that sweatpants, bras, and leggings can be considered essential wear, the cost of its products places them in a more premium category.

That’s beneficial for profit margins, but it implies the company must meet a different level of expectation compared to, for example, clothing labeled as Champion.

Quality errors, which have occurred previously, can turn into a public embarrassment forthe retailer. Mistakes in fashion can also lead to negative attention. Both situations may cause customers to seek out other brands for their style needs.

Being a popular brand has significantly boosted Lululemon, but don’t overlook the other side of this situation if you’re considering the stock. The financial success of this retailer will depend on the ever-changing preferences of its customers. Trends in fashion, economic downturns, and customer boredom could all impact the company’s performance.

Its insufficient direction for the latter part of 2025 was emphasizedtariff issues. However, same-store sales(comps) in the Americas declined by 4%, indicating that the brand might not be connecting as effectively as anticipated at this time.

2. Lululemon has two approaches to growth

The limited direction for the remainder of 2025 resulted in a rapid drop in the stock price. This is not unexpected, but comparable performance is not the sole key factor when evaluating Lululemon’s potential for growth.

Comps evaluate how stores that have been open for a minimum of one year are faring. It is an essential indicator of the business, but Lululemon is highly profitable, and itsbalance sheetHas no long-term debt and more than $1 billion in cash. It has ample time to address fashion challenges, even though these can lead to significant earnings issues in the short term.

Another approach to expansion involves launching additional locations. During the second quarter of 2025, the company added 14 new stores, increasing its overall number of locations to 784.

New outlets significantly contribute to the revenue ofthe income statementand can offset weak comparable sales figures. This occurred in the second quarter, with revenue in the Americas increasing 1% despite the weakness in comparable sales.

Then there’s the company’s international opportunity, where comparable sales are still robust, and there remains significant potential for additional locations. To quantify this, comparable sales in the international segment increased by 15%, with total sales in that division rising 22%.

A difficult period is unlikely to make Lululemon a poor business, even if a weak phase causes Wall Street to react negatively to the stock.

3. The decrease in price makes the stock appear (relatively) inexpensive

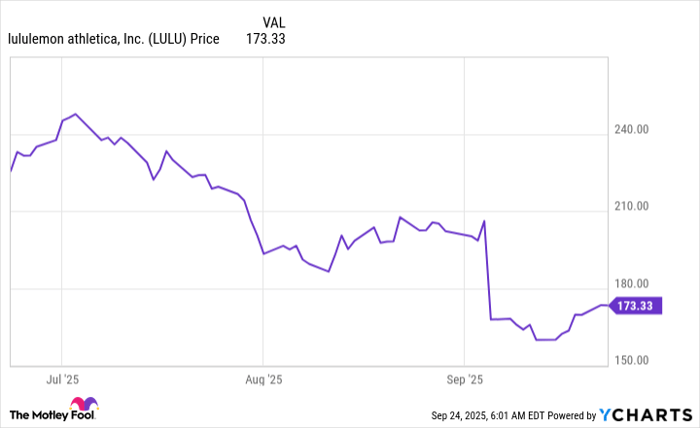

The core of the story revolves around valuation, as Lululemon’s stock has dropped by approximately two-thirds since reaching record highs in late 2023. To be honest, significant declines are common for the stock, having experienced several drops of 40% in the past. However, a 66% decline is quite substantial, with only one comparable drop occurring early in its history.

Examining the company’s valuation indicators following the recent significant drop in price indicates that the stock is currently undervalued. Itsprice-to-sales, price-to-earnings, and price-to-book-value ratios are all significantly lower than their five-year averages.

For more-aggressive investors with a growth focus, that could present a chance. Those who have faith in ggrowth at an affordable cost(GARP) could also find the narrative interesting.

Ensure you are aware of what you are purchasing from Lululemon

Lululemon is going through a challenging time, but it remains a solid company. It has the potential to expand its retail locations while addressing its style-related challenges.

If you’re a long-term investor capable of managing the fluctuations associated with owning a premium, trend-focused retailer, it might be a worthwhile investment. However, if you prefer a more cautious approach, Lululemon’s fundamental business strategy may not align with your investment style.

Is it a good idea to invest $1,000 in Lululemon Athletica Inc. at this moment?

Before purchasing shares in Lululemon Athletica Inc., keep this in mind:

The Motley Fool Stock Advisorthe analysis team has recently recognized what they think are the10 best stocksFor investors to purchase now… and Lululemon Athletica Inc. was not among them. The 10 stocks that were selected have the potential to deliver significant returns in the years ahead.

Consider when Netflixcreated this list on December 17, 2004… if you had invested $1,000 at the moment of our suggestion,you’d have $652,872!* Or when Nvidiacreated this list on April 15, 2005… if you had invested $1,000 at the moment of our suggestion,you’d have $1,092,280!*

Now, it’s worth noting Stock Advisor’sThe overall average return is 1,062% — a significant advantage over the S&P 500’s 189%. Don’t overlook the newest top 10 list, which is available upon joining.Stock Advisor.

View the 10 stocks »

*Stock Advisor results as of September 22, 2025

Reuben Gregg Brewerdoes not hold any position in the stocks mentioned. The Motley Fool holds positions in and recommends Lululemon Athletica Inc. The Motley Fool has adisclosure policy.