This installment of Reputation Managementis not as focused on narrative and instead emphasizes examining current events in the automotive sales industry in an original way. — Sajeev

Regardless of your race, religion, or skin color, we face an issue known as “credit invisibility” in zip codes throughout the country. This term, as defined by the Consumer Financial Protection Bureau, refers to an individual who “does not have any credit history with one of the three national credit reporting agencies.” I have previously highlighted the importance of addressing this problem.to come to terms with these companiesin the first part ofReputation Management, particularly when the industry that serves those who are credit invisible is not always acting in their customers’ long-term best interest.

The sector is typically referred to as “Buy Here Pay Here” (BHPH), as they provide financing for their customers. In contrast, a standard dealership usually transfers most of this responsibility to a reliable lender, often major banks with well-known reputations. Both approaches have advantages and disadvantages, but bank financing tends to be more beneficial for long-term credit and financial stability. Although we previously examined the quality of vehicles available at BHPH dealerships, these businesses serve an important role in helping individuals without a credit history obtain a vehicle. However, not all such dealers are the same.

A major BHPH dealer named Tricolor has recently applied for Chapter 7 bankruptcy. (This is the type that involves selling off assets, not restructuring.) If you come across any news about Tricolor in traditional media, it’s likely to focus on their customers’ immigration status. That’s a sensitive political issue I’d rather not get involved with, so let’s instead examine their branding: The name Tricolor seems intentionally chosen to remind people of the green, white, and red colors of the Mexican flag.

This approach allows this major BHPH to quickly establish a bond with customers that smaller, local “mom and pop” stores typically take years to build through word-of-mouth and trust. They also have the financial resources to acquire abandoned new car dealerships located along highways. Applying the Tricolor brand to these dealerships provides the company with a straightforward way to address the Four P’s of marketing: products, place, price, and promotions.

But there’s another “P” in Tricolor’s marketing success: Precedent. While Glenn Bell (known for Taco Bell) tried tacos fromMitla Cafeand transformed it into a fast food business, Tricolor sold approximately 35,000 pre-owned cars last year to their distinctive, overlooked customer group.

This was impressive, at least in theory. Tricolor CEO Daniel Chuonce said his company’s use of big datadeveloped something that genuinely functions as a credit bureau for undocumented Hispanics who lacked any actual bureau data.

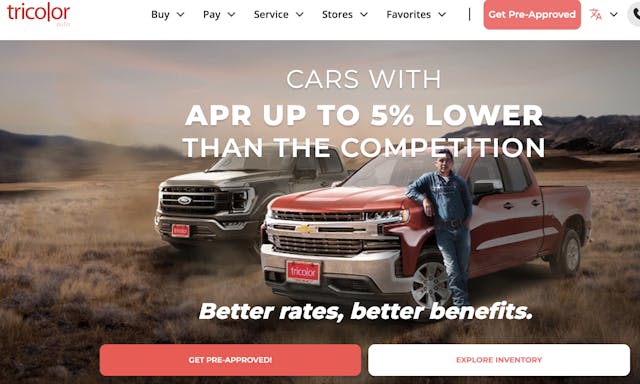

By utilizing pay stubs and records of rent payments instead of a credit score, Tricolor developed a method to evaluate potential customers, then set an APR for their loans based on their own judgment. If the screenshot below is accurate, they have significant flexibility in their self-funding approaches.

Where else but on a BHPH website would you find a car dealership promoting interest rates?possibly lowermore than their competitors, let alone by five percentage points? Chu’s application of Big Data provided investors with a strong rationale to back Tricolor’s efforts with the Credit Invisible, and Tricolor managed to convince three banks to provide them with warehouse loan underwriting. Unfortunately, they are alleged (allegedly!) utilized the same collateral for every loan, resulting in a downward cycle leading to Chapter 7 liquidation.Car Dealership Guywrote a solid piece on this topic.

There is online discussion about Tricolor’s collapse indicating larger issues with subprime lending, yet many dealerships are thriving in this area. Only one has faced trouble due to financial misconduct. Even CarCountry, the company where I work as a Reputation Manager, once explored this market.

***

It’s currently the late 2010s, and I was surprised to discover that my large multinational company, CarCountry, officially reported selling more pre-owned vehicles than new ones in the previous year. This was partly due to their new selection of used cars designed for customers with poor credit histories.

It turns out that CarCountry was an unspoken part of the same movement that caused Carmax’s stock to surge during this period. Their supply of used vehicles became ideal inventory for this income source. However, they remain a franchise dealership group with ethical guidelines (whether due to oversight from Wall Street or the original equipment manufacturers), so they used third-party financing (not a BHPH business approach) because of subprime lending.was officially back in style with their banking buddies.

Lauren, my Reputation Management assistant, didn’t enjoy what she was seeing in our company’s press statement. She raised some legitimate issues:

Why are we offering these subpar used cars for sale? Wouldn’t it be more beneficial to sell them through an auction and concentrate on more lucrative pre-owned, certified pre-owned, and new vehicles?

What an intriguing question! I was certain I had hired Lauren for a solid reason. I clarified that CarCountry would generate significant profits on every sale, as they only reconditioned SSS-tier (stop, steer, start) vehicles to meet street legal standards and qualify for subprime banking. Although I had no idea just how lucrative the loan origination fees were for the subprime loans CarCountry produced, I advised Lauren that this particular endeavor was definitely worth the effort.

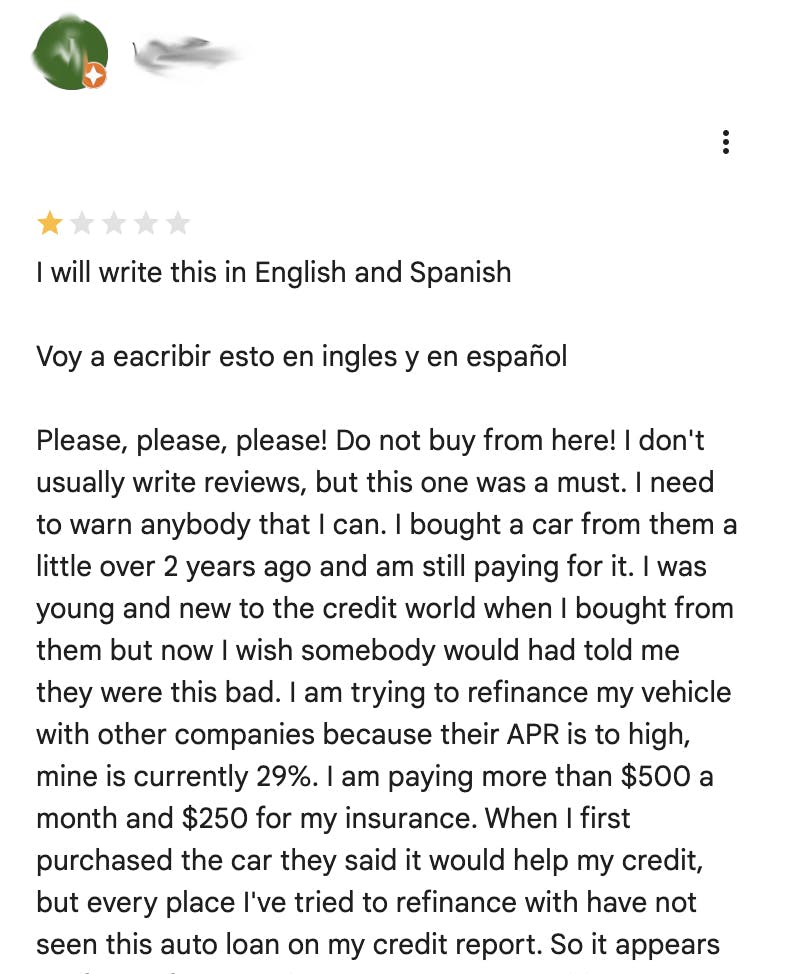

It seems that CarCountry also successfully sold extended warranties with these SSS vehicles (which could have been a smart decision!), but I still made it clear to Lauren that we were not becoming a BHPH company. This turned out to be beneficial for all parties involved, as CarCountry provided a bank loan that ensures the customer.an opportunity to establish credit. It wasn’t long before a review from a Tricolor customer highlighted the importance of this distinction.

Occasionally, the most persuasive arguments originate from a dissatisfied customer, which helped ease Lauren’s worries about her work environment. Although we encounter some extreme cases on CarCountry review sites, her recent experience purchasing her first car highlighted how distinct these two dealerships are in representing the customer’s interests.

It was just a year ago when Lauren bought a pre-owned Chevrolet HHR SS, a vehicle I insisted she purchase before leaving our local CarCountry dealership. And I really meant it when I said I demanded it, since I wanted to drive it during our lunch breaks. My reasoning was valid because she needed a more dependable car, and this one had a clean CarFax report, had only one owner, and could enter “Launch Control” mode for a powerful acceleration at traffic lights.

Lauren laughed happily when I showed her that feature on a small road behind the dealership. The OEM Goodyears protested as the turbo pushed us forward, indicating their current condition was barely adequate. I collaborated with the used car manager to locate high-quality replacement tires in CarCountry’s inventory management system (DealerTireIt was an impressive maneuver, and they incorporated them into the deal with a slight increase in her monthly payment. My task was complete, and my colleagues hinted that I might have a promising future in sales, just in case Reputation Management ever disappears.

Without going into excessive detail, Lauren’s used car purchase was quite different from the Tricolor review mentioned earlier. She worked with a major bank, signed documents for a low APR loan, and took advantage of employee discounts that made obtaining a lively HHR feasible for a younger buyer with a limited credit history. Lastly, an HHR of this quality (apologies for the pun) would never end up on a BHPH lot, as it perfectly represented a clean dealer trade-in.

Although not every detail in that Tricolor review may be accurate, it’s definitely credible. Particularly the section regarding financing at 29% APR. Lauren was shocked that it was legal for someone to have an APR 21 percentage points higher than hers. Now that she is aware of this, I requested the proper response from Tricolor’s Reputation Manager. (Tricolor didn’t have the courage to reply to this thoughtful review.)

I wouldn’t reply to that either. I’d be searching for a new position as well.

Wise words, Lauren. Wise words. It seems your manager has taught you well, and he will claim credit for this. Just as he did with the HHR SS.

The Public Image Specialist will return…

The post Reputation Control: These Colors Run appeared first on Hagerty Media.

Want to buy a car? Discover the perfect one on the MSN Autos Marketplace.